bank owned life insurance tax treatment

More Company-Owned Life Insurance COLI. However if they may be surrendered for their cash surrender values.

Irs Foreign Life Insurance Policy Taxation Is Income Taxable

The bank generally pays the entire premium and is the beneficiary.

. The face amount of the policy if specified in the policy. 5000 Life Insurance income account. Tax treatment is changed existing plans may be grandfathered.

These premiums are also not tax-deductible. When the death of a bank officer or other key person would be of such consequence to the bank as to give it an insurable interest key-person life insurance insures the bank on the life of the individual. Many businesses own life insurance on employees and owners and designate the business as beneficiary of the policy.

The sweeping Tax Cuts and Jobs Act TCJA signed into law in late 2017 includes a provision that appears to apply to bank-owned life insurance BOLI which often is used as a tax-free investment for banks sometimes but not always coupled with an employee benefit program. The tax treatment of proceeds paid on the death of the insured is unaffected by the fact that the contract is a MEC. In the past money received through a life insurance contract paid by reason of the death of the insured were generally not includable in gross income for federal tax purposes.

However The Pension Protection Act of 2006 enacted important statutory changes to the general rule for employer-owned life insurance contracts stating that death benefits received. Corporate Owned Life Insurance COLI owned by banks is often referred to as Bank Owned Life Insurance or BOLI. They do this in order to protect the entity from the loss of a key person or to.

Executive Benefits Network has helped. While progress toward reform of the Internal Revenue Code IRC may slow in light of the upcoming congressional midterm elections a proposal that. Key-Person Versus Split-Dollar Life Insurance Key-Person Life Insurance.

If you are receiving the proceeds in installments whether there is a refund or period-certain guarantee. Bank Owned Life Insurance BOLI Bank Owned Life Insurance BOLI is defined as a company owned insurance policy on one or more of its key employees. Understanding its impact on the financial statements of your business is an important element in making a decision on the use of a business owned life insurance policy.

But there are times when money from a policy is taxable especially if youre accessing cash value in your own policy. In general proceeds from life insurance policies are tax free under the general exception rules in Sec. Cash surrender values grow tax-deferred providing the bank with monthly bookable income.

Life insurance payouts are made tax-free to beneficiaries. The tool is designed for taxpayers who were US. Bank-owned life insurance is bought by banks as a tax shelter leveraging tax-free savings provisions to fund employee benefits.

The new section limits the amount of tax-free treatment a person which can be any type of entity can. The primary purpose of this type. The tax treatment of corporate-owned life insurance COL I continues to receive scrutiny from congressional tax writers and the Obama Administration.

If an employer pays life insurance premiums. Bank Owned Life Insurance BOLI is the predominant investment asset for financing the cost of employee benefit plans. There are important distinctions however in how this term BOLI may be used that should be understood.

If the tax treatment is changed existing plans may be grandfathered. The bank purchases and owns an insurance policy on an executives life and is the beneficiary. 101 j 1 was added with the enactment of the Pension Protection Act of 2006 PL.

Rulings concerning the federal income tax consequences regarding the recognition of a loss on the surrender of bank owned life insurance BOLI submitted by Taxpayer. Bank Owned Life Insurance BOLI is a tax efficient method that offsets employee benefit costs. The tax issues associated with key person term life insurance are relatively unambiguous.

What are the requirements for deductibility. Heres how it works. In order for all or a part of premiums payable on an insurance policy to be deductible the following requirements must be met in accordance with.

Life Insurance premium expense account. National banks may purchase and hold certain types of life insurance called bank-owned life insurance BOLI under 12 USC 24 Seventh. Citizens or resident aliens for the entire tax year for which.

Life insurance premiums under most circumstances are not taxed ie no sales tax is added or charged. A life insurance policy used as collateral security may be an allowable deduction under paragraph 201 e2 of the Income Tax Act the Act. The new provision could have unintended consequences for bank mergers and.

Taxpayer qualifies as a bank within the. However if existing policies are not grandfathered they may be surrendered for their cash surrender values. If federal income tax was withheld from the life insurance proceeds.

Banks can purchase BOLI policies in connection with employee compensation and benefit plans key person insurance insurance to recover the cost of providing pre- and post-retirement employee benefits insurance on borrowers and. Upon the executives death tax-free death benefits are paid. This general rule changed when Sec.

FACTS Taxpayer is a national banking association and is wholly owned by Parent a holding company and bank holding company. If the taxpayer is directly or indirectly a beneficiary under the policy or contract The tax treatment of death benefits associated with such a. A 2006 change in tax law caused employer-owned life insurance benefits to become taxable if the employer lacks the correct documentation.

3200 Conclusion The use of Life Insurance may be a key financial decision for your business. 264 a 1 provides No deduction shall be allowed for premiums on any life insurance policy.

:max_bytes(150000):strip_icc()/hsbc-branch-in-new-bond-street--london-533780165-ff99ebc393c243cba463ea80559836b0.jpg)

Bank Owned Life Insurance Boli

Bank On Yourself Using Life Insurance As A Source Of Liquidity Nerdwallet

Cash Flow Banking With Whole Life Insurance Explained

2

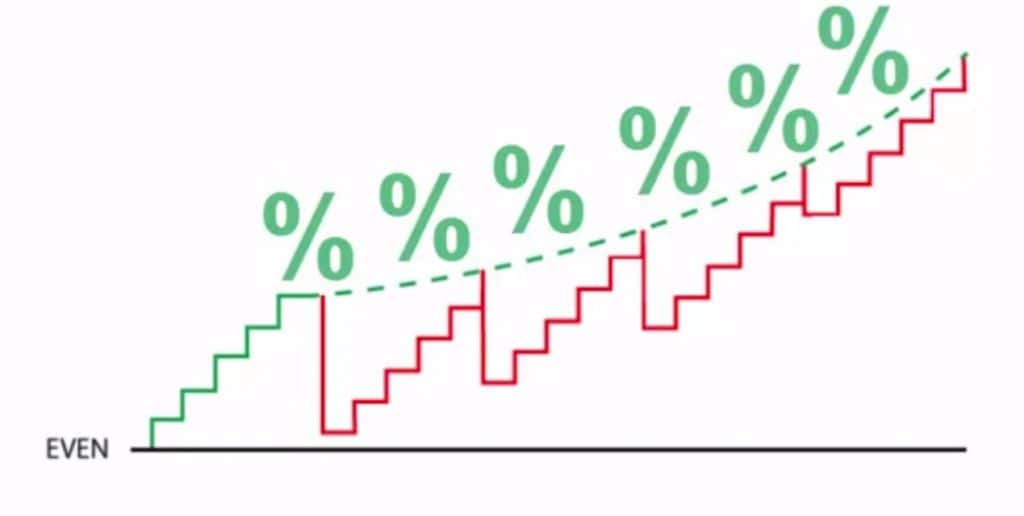

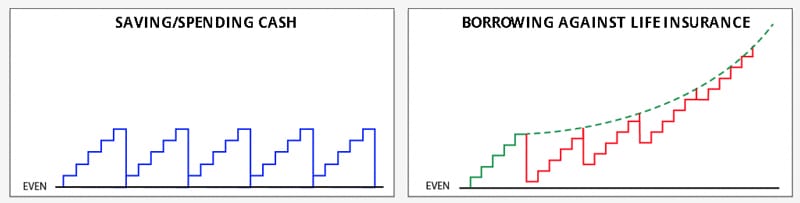

5 Steps To Be Your Own Bank With Whole Life Insurance Banking Truths

5 Steps To Be Your Own Bank With Whole Life Insurance Banking Truths

/dotdash-variable_universal-Final-66a32d4c8d84418ab1271e02d73d2a4b.jpg)

Variable Life Vs Variable Universal What S The Difference

Key Man Life Insurance What Is It How Does It Work 2022

Understanding Life Insurance Policy Ownership The American College Of Trust And Estate Counsel

Tax Deductible Life Insurance Business Owners

Do Beneficiaries Pay Taxes On Life Insurance

/dotdash-090816-cash-value-vs-surrender-value-what-difference-final-b2df392375e34caf9eac4e7bc2648283.jpg)

Cash Value Vs Surrender Value What S The Difference

Tax Deductible Life Insurance Business Owners

![]()

Norway S Follow Up Of Agenda 2030 And The Sustainable Development Goals Regjeringen No

Life Insurance As A Tax Planning Tool Insights People S United Bank

Pin On Vault Of Knowledge

5 Steps To Be Your Own Bank With Whole Life Insurance Banking Truths

Is Life Insurance Taxable Forbes Advisor

Bank Owned Life Insurance Boli